We might learn about inflationary periods in books or news, but we definitely experience it at the grocery store. We know inflation is a macroeconomic phenomenon that gradually reduces the value of money, leading to a constant increase in the cost of goods and services, directly impacting saved funds and all sectors of the economy in general.

Today, we’ll focus on how to deal with inflationary periods while investing so we can determine the best investment during inflation.

Investments and Inflation

When prices rise, the purchasing power of our money decreases and our cost of living increases. If you keep your money in your bank account (or in cash), you are losing money.

That’s why it’s necessary to seek assets that can preserve the value of our wealth. Ideally, your investments should have higher returns than the inflationary index. But we know this isn’t always the case, nevertheless, you are still in a more favorable situation than those who don’t invest. You don’t want to see the value of your money decreasing in front of your eyes.

To learn how your money loses value over time due to inflation check our previous article.

There are a lot of sectors where you can invest, we will recommend a few.

The best investments during inflation

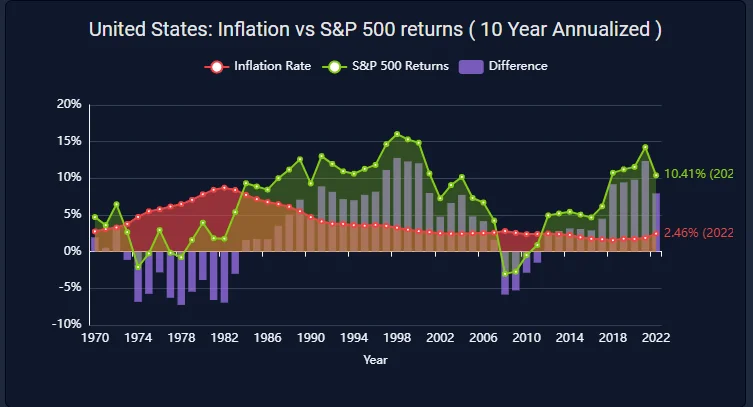

Stocks: the best strategy against inflation. Historically, 78% of the time stocks outpaced inflation, more times than a bond portfolio. Even the fall down that stocks may have by product of the increase in interest rates, is followed by a comeback from the loss, eventually surpassing the inflation levels. It’s important to consider companies with growth potential, companies with strong pricing power and companies that can raise their prices in response to inflation, which can lead to higher revenues and profit.

Real estate or REITs: property is a finite resource, and as the cost of goods and services rises, so does the value of land and buildings. You can invest in real estate directly – which requires a higher first investment and higher maintenance costs. Or through a REIT (Real Estate Investment Trust); over the last decade, the MSCI U.S. REIT Index has had an average annual return of more than 10%.

Commodities that work as value reserves: precious metals, like gold and silver, tend to rise in value -because of their durability and rarity- as inflation increases, providing a shield against the erosion of the purchasing power of money. This is why they are good options for keeping value during inflationary periods.

TIPS (Treasury Inflation-Protected Securities): government-issued security bonds designed to adjust with inflation levels. Their unique structure allows them to adjust payments based on the inflation data; if inflation increases the interest rate you earn on these bonds increases as well, ensuring that you maintain your purchasing power even when the general price level is increasing.

The worst investments during inflation

As well as there are the best, there are some assets we wouldn’t recommend you:

Cash or savings: in inflationary periods, the value of cash diminishes as inflation increases and the cost of living augments, resulting in a loss of wealth for those who hold large amounts of cash. If you have your savings in a bank account it’s the same story.

Fixed-rate debt securities: the income they generate remains constant, regardless of changes in inflation, so when inflation increases, the purchasing power of the interest payments diminishes. For example, if you own a bond that pays 3% annually and inflation rises to 6%, the real return on your investment is negative, as the income generated is not enough to keep up with the increased cost of living.

Companies with weak pricing power: companies that cannot pass on their costs to consumers by raising the prices of their goods and services when their costs increase due to inflation. If they do increase their prices, demand for their products decreases because there are multiple substitutes available on the market.

Commodities that don’t work as value reserves: agricultural products like corn or coffee are not a good idea to invest in during periods of inflation because they are perishable, which affects their long-term value. Also, their prices can be highly volatile, influenced by seasonal changes, weather conditions, and short-term supply and demand fluctuations.

Conclusion

Navigating the financial landscape during inflationary periods requires careful consideration of how different assets respond to rising prices. As we’ve discussed, inflation can erode the purchasing power of money, making it essential for you to strategically invest your money to maintain and grow your wealth.

On the one hand, assets like stocks, real estate, commodities, and TIPS consolidate as the best investments during inflation. These tend to either appreciate in value or offer returns that outpace inflation, making them effective tools for preserving wealth.

On the other hand, holding large amounts of cash or investing in fixed-rate debt securities are bad ideas during inflationary periods, as these assets typically lose value in real terms when prices rise. The key is to focus on investments that either directly benefit from inflation or have built-in mechanisms to adjust for it.

In conclusion, stocks consolidate as the best investment during inflation. With the power of compound interest, a diversified portfolio, and the adherence to a long-term investing plan you can not only go through market fluctuations but also win against inflation and preserve or augment your wealth.

If you want to start investing in a friendly platform with the help of professionals and beat inflation, join us.

The investment world is one in which theory and practice go hand in hand, but it is very important to consider also the psychological aspect of value investment, it requires patience and discipline not to get caught up in the trap of instant gratification and to resist the market fluctuations. That’s what we will focus on today, the psychological aspect of value investing: patience and discipline.

Psychological challenges – The impact of fear and greed

Fear and greed are two of the most powerful emotions that can significantly influence investment decisions, often leading investors to buy or sell at the wrong time. Markets can be volatile and unpredictable. Prices can fluctuate wildly in response to various factors, such as economic indicators or geopolitical events. During these turbulent times, it is tempting to react impulsively and make irrational decisions based on short-term market movements.

On the one hand, fear normally appears during market downturns, and it can cause investors to panic and sell off assets at a loss, even when most of the conditions that motivated the investment in the first place remain solid. This irrational behavior is driven by a desire to avoid further losses, but it often results in missing out on potential recoveries. The cyclical nature of markets means that downturns are usually followed by recoveries, and selling in a panic can lock in losses that would otherwise be temporary.

On the other hand, greed can drive investors to take unnecessary risks, especially during bullish markets. The fear of missing out (FOMO) can lead to overconfidence, pushing investors to buy overvalued stocks in the hope of quick profits. This behavior is often seen during market bubbles, where the desire for rapid gains blinds investors to the underlying risks. Greed can also result in holding onto winning positions for too long, ignoring signs that it might be time to sell. This can lead to significant losses when the market eventually corrects.

There are three concepts that can explain this behavior:

Loss aversion. People fear losses more than they appreciate gains. About this, there is a very interesting article that critiques the expected utility theory as a descriptive model of decision making under risk written by nobel prize winners Daniel Kahneman and Amos Tversky in 1979. It’s called “Prospect Theory: An Analysis of Decision under Risk”.

Overconfidence. People tend to believe their abilities and knowledge are better than they actually are, undertaking risky investments, thinking they can outsmart the market.

Anchoring. People rely heavily on an initial piece of information (the “anchor”) to make decisions, ignoring other important factors that can determine the best move.

Be patient.

In the world we live in, where instant gratification seems to be the norm, being patient is a challenge that requires strength, some kind of strength that is trained in a process of introspection and self-discovery that goes hand in hand with practical habits.

We know financial markets are volatile and inherently cyclical, experiencing periods of rapid growth followed by corrections or downturns. Being patient in these moments is crucial. Instead of succumbing to fear and selling off assets during market drops, recognize these corrections as opportunities to purchase undervalued stocks at lower prices. By remaining patient and strategically investing during these downturns, you can acquire high-quality assets at a lower cost, positioning yourself for substantial gains when the market eventually recovers.

Patience equals focus on the long-term perspective. By patiently waiting for the value of an investment to appreciate over time, investors can potentially unlock substantial returns. Don’t forget about the benefits of the compound interest and how it works: by holding investments over an extended period, the returns generated each year are reinvested, leading to exponential growth and substantial wealth over time.

When you focus on the long term, you aren’t perturbed by daily market fluctuations. You don’t anxiously check your portfolio every few minutes, and you don’t lose sleep over a single bad day in the market. Your mental peace isn’t held hostage by the unpredictable movements of the market.

Have discipline.

The same goes with discipline, it’s another cornerstone of successful value investing that requires strength and training. It is easy to get swayed by short-term market fluctuations that can trigger strong emotional responses, leading to rash actions such as panic selling during downturns or overbuying during bullish periods. Such reactions conclude in impulsive investment decisions that often result in financial losses and missed opportunities.

Discipline helps you avoid emotional or impulsive decisions, and keeps your focus on the objective that motivated the whole process in the first time. But it doesn’t only aid in achieving financial objectives, it also builds a mindset of stability and confidence. A mindset that will help you get through market’s (and life’s) ups and downs.

It begins with establishing clear investment criteria and adhering to them consistently, regardless of the market noise. By choosing an investment strategy like dollar cost average you are regularly investing a fixed amount of money into the market, despite its current state.

Keep in mind that discipline is not about suppressing emotions, but about acknowledging them and, at the same time, not allowing them to cloud your judgment.

A clear example of the rewards of discipline and patience in investing is the recovery of the stock market after the 2008 financial crisis. Investors who remained patient and disciplined while continuing to invest during the downturn saw significant returns as the market rebounded in subsequent years.

How to manage this psychological aspect

Managing the psychological aspect of value investing is crucial for maintaining a clear and focused mind. Mindfulness and stress management play a significant role in this process.

Mindfulness involves being present in the moment and aware of one’s thoughts, emotions, and surroundings – without judgment. In inversions, this means staying conscious of market movements and your own reactions to these changes without immediately reacting.

Stress management techniques are equally important to deal with the volatility and uncertainty of the stock market. Regular practices such as meditation, deep breathing exercises, and physical activity can help reduce stress levels and improve overall mental health. These activities help to calm the mind and body, allowing you to approach your decisions with a clearer perspective and reduced emotional interference.

By managing stress effectively and by practicing mindfulness, you can gain better control over your impulses, making it easier to have the patience to stick to the long-term investment strategy and have the discipline to avoid impulsive decisions driven by fear or greed.

Remember that incorporating these practices into an investing routine not only enhances decision-making but also contributes to a healthier and more balanced life. If you regularly practice these techniques, you will be better equipped to handle the emotional ups and downs of the market.

How TBI can help you

At TBI we truly believe in the importance of dealing with the psychological aspects of value investing: patience and discipline; as mentioned. And that’s why our service is articulated to help you. From reminders and alerts that we send you to keep track of your investment plan and to help you make decisions without being influenced by psychological factors, to our robust algorithm that allows you to gain confidence in the process to keep moving forward, and much more. We aim to make this apparently difficult process as friendly as possible. Don’t wait any longer and join us: https://theboringinvest.com/#/investment-board

Conclusion

On the surface, investing appears to be all about numbers, data and cold hard facts. However, those who explore its depths realize that investing is both a psychological journey and a financial one. It’s a perpetual dance between fear and greed, between the desire for immediate gratification and the discipline of patience.

Both fear and greed undermine the core principles of value investing, which emphasize patience and discipline. To be successful in this amazing practice of value investing, advocate for a long-term perspective and focus on the intrinsic value of investments rather than short-term market fluctuations or the momentary stock prices.

Overcoming these emotional challenges that surround inversions requires discipline, implying setting clear investment criteria and adhering to them regardless of the stock market conditions. That’s how you make rational decisions that align you with your long-term financial goals.

We hope to have made clear the importance of the psychological aspect of value investing: patience and discipline give you the fortitude to withstand short-term losses for long-term gains. Remember that “investing is a marathon, not a sprint”.

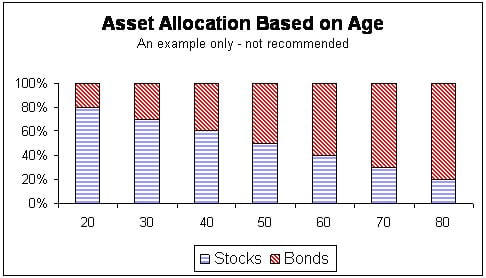

There are several approaches when it comes to portfolio adjustment or asset allocation determination. The best one may depend on specific financial circumstances, risk tolerance, financial objectives, and investment time horizon. Today, we bring you Benjamin Graham’s formula (100 minus age) so you can decide the number of stocks most convenient for you to own according to your age. Let’s learn how you can adjust your portfolio with Graham’s formula and how many stocks you should have according to your age.

Graham’s formula

First of all, let’s make clear what asset allocation means: it’s how investors divide their portfolios among various asset classes such as stocks, bonds, cash, commodities, real estate, etc.

Now, Benjamin Graham is a well-known figure in the investments realm because of his contributions to the community; among his books, we remark The Intelligent Investor, in which he proposes his famous formula “100 minus age”. It consists of subtracting the number of your age in years to 100 and using the result as the percentage of stocks you should invest in.

If you are 30 years old, the formula comes to 100 – 30 = 70 so the 70% of your investment portfolio should be in stocks, the other 30% could be in bonds or other assets. This approach suggests a major exposure to stocks in the youth, when more risk can be tolerated, and a major security in bonds (or other more stable assets) as the investor ages. By the way, this doesn’t mean that stocks can’t be safe, as we explained in a previous article.

Age-Based Investment Strategy

In your 20s and 30s, you have a longer time horizon for your investments to grow, allowing you to take on more risk with a higher proportion of stocks. Stocks typically offer higher returns compared to bonds, making them ideal for younger investors aiming for aggressive growth. At this stage, it’s crucial to diversify your stock investments to maximize potential gains while mitigating risks. Although bonds might play a minor role in your portfolio, their inclusion can still provide a safety net against market volatility.

As you approach your 40s and 50s, your investment strategy should begin to shift towards a more balanced approach, gradually increasing your allocation to bonds. This transition helps to protect the wealth you’ve accumulated while still allowing for growth through stock investments.

In your 60s and beyond, the primary focus of your investment strategy should be on preserving capital and ensuring a steady income stream. This means significantly increasing the allocation to bonds, which offer lower risk and more predictable returns compared to stocks. The emphasis should be on low-risk investments that safeguard your retirement funds.

Advantages and Disadvantages

On the one hand, one of the evident advantages of this formula is the simplified investment decision-making, as it provides a clear and easy-to-follow guide for investors seeking proper asset diversification. It notably helps balance risk and increase financial security; by reducing the number of stocks over time, it decreases volatility and protects accumulated capital.

On the other hand, one of the main disadvantages is that it does not take into account the individual circumstances of the investor, such as their specific financial goals, personal risk tolerance, and economic situation, nor does it consider market dynamics and changes in the economy. We know that these factors can profoundly affect the performance of our investments.

Conclusion

As we saw, it’s very simple how you can adjust your portfolio with Graham’s formula and how it works to determine how many stocks you should have according to your age; it just comes down to subtracting the investor’s age from 100 to determine what percentage of your portfolio should be invested in stocks. It’s a simple and accessible approach for investors seeking to balance risk and security in their portfolios throughout their lives.

It can be very useful as a starting point or as a general rule (rather than a golden rule) to apply in moments of confusion. However, it is important to understand its limitations. Ultimately, the key to a successful investment strategy lies in balance and continuous adaptation to individual needs and market dynamics.

Nowadays, we know that the best way to become wealthy is by working with money itself. There are various approaches -some contradictory, others complementary- on how to use money to build wealth. Today, we will analyze two viewpoints from two well-known figures in the financial community, they seem contradictory and incompatible. So, who is right about how to get rich? Robert Kiyosaki or Dave Ramsey?

Robert Kiyosaki

Let’s start with the author of the Best Seller Rich Dad, Poor Dad. The first rule that appears in his book is “don’t work for money”, this means: don’t stay in a job that allows you to live paycheck to paycheck, instead, you should get debt and invest – but not in the stock market. This may sound odd, let’s explain it in more detail.

In a 2020 interview, Kiyosaki stated that he doesn’t care about money, yet he still makes money because he understands the system. By “system,” he refers to the contrast between how money actually works and the socially accepted lie about it.

Society sets a trap for us by saying: “go to school, get a job, work hard, buy a house, save money, pay taxes, and invest in the stock market.”For Kiyosaki, that makes you poor. Instead of being educated through institutionalized education, he promotes “studying money” and taking on debt to avoid having to work in economic dependency.

We acknowledge that it is important to understand and critique the system, but we find his stance somewhat exaggerated. These are strong, controversial statements, that can be subjected to critiques such as the following:

Critics to Kiyosaki’s approach

Not everybody can borrow money to buy assets, there are some limitations inherent to the financial system, for example, it’s a possibility that you don’t pass the requirements to get a loan because there are some very specific warranties and probably high interests that require sufficiently good assets to return the money and avoid bankruptcy.

Kiyosaki also said that you shouldn’t invest in the stock market. But the reality is that stocks are business, all you have to do is look for a profitable business that will return the investment you made in the shortest period of time possible. The fascinating thing is that buying stocks allows you, while being a normal person, to buy a part of any business of your interest (as long as it runs in the stock market).

Dave Ramsey

Furthermore, Dave Ramsey is a well-known figure in the investment world, even though he has a radically different viewpoint from Kiyosaki.

Dave Ramsey summarizes what anyone seeking to build wealth through good personal financial management should do in 5 steps:

1st You need to have a written plan, a budget. Because no one accidentally wins.

2nd Get out of debt. When you don’t have any payments, you have money.

3rd Live on less than you make. If you are spending more money than you earn, you need to reconsider your spending habits or your sources of income.

4th Save money. Savings are fundamental to have a backup in case something doesn’t go as planned or something unexpected occurs, and to have a solid base to start investing with.

5th Be outrageous with money.

We think that this approach to investments makes it more accessible for common people like us to embark on a process of economic growth by trusting that our most valuable assets -time and money- are invested correctly.

Conclusion

As we made clear, there are some fundamental differences between Robert Kiyosaki and Dave Ramsey in terms of the strategy they believe in in order to get rich.

On the one hand, Kiyosaki believes in not saving, taking debt, and investing in business (not stocks). On the other hand, Ramsay believes in saving money, getting out of debt, and investing in stocks.

Even though Kiyosaki’s knowledge and experience is something to take seriously, in TBI we go with the Dave Ramsay approach, and that’s what we recommend to you: save and invest. That’s how you manage your money to become wealthy.

There is a wide variety of strategies, approaches, and manuals that can be applied when it comes to investing. And while each investor has their style, determined by their goals, financial profile, and experience in the field; some strategies prevail and dominate over time due to their high efficiency. Today we will focus on one of the best investment strategies, simple and suitable for anyone, even more important for beginners. It’s called “dollar cost averaging” (DCA).

What is the Dollar Cost Average? AndHow does it work?

Dollar Cost Average means investing for the same amount of money each month or each quarter, while the alternative option would be to invest it all in a single point in time. You can already predict what are the main advantages and disadvantages of DCA, and we will explain in this article why we highly recommend DCA.

If applied in common stocks, as the number of shares that can be bought for a fixed amount of money varies inversely with their price (the higher the price per share the lower the amount of shares you can buy with a fix amount), DCA effectively leads to more shares being purchased when their price is low and fewer when they are expensive. As a result, DCA can lower the total average cost per share of the investment, giving the investor a lower overall cost for the shares purchased over time.

There are only two parameters that the investor needs to decide when implementing this strategy: the fixed amount of money available to invest each timeand how often the funds are invested. This leads to an automatic investment system that doesn’t require much time, expert judgment and knowledge.

To have success with DCA it doesn’t matter the actual price of the stock nor the tendency. Regardless of that, the effectiveness of the method relies on the investor, who should respect the previously determined amounts and periods of investment. There’s no other secret than planification, perseverance, and a little patience.

Benjamin Graham, a man of renown in the field of investments, was the one who first coined the dollar cost average term. He said in his book The Intelligent Investor(Warren Buffet’s favorite book): [DCA] “means simply that the practitioner invests in common stocks the same number of dollars each month or each quarter. In this way he buys more shares when the market is low than when it is high, and he is likely to end up with a satisfactory overall price for all his holdings.”

Practical example

Let’s suppose an investor decides to allocate $100 each month to invest in a fund tracking the S&P 500 index, which trades at different prices each month.

In the first month, the fund’s price per share is $50, so with the $100, the investor buys 2 shares of the fund.

In the second month, the price per share of the fund decreases to $40. With the other $100, the investor buys 2.5 shares.

In the third month, the price per share increases to $60. With the $100, the investor can only buy 1.67 shares.

After three months, the investor has invested a total of $300 and has acquired a total of 6.17 shares of the fund. If we sum the number of shares purchased and calculate the average cost per share, we find that the weighted average cost per share is approximately $48.53.

This example illustrates how dollar cost averaging allows the investor to buy more shares when prices are low and fewer when prices are high, resulting in a lower average cost per share compared to if they had invested a fixed amount at a single point in time.

Advantages and disadvantages of DCA

Let’s start with a disadvantage of DCA regarding transaction costs: the repeated investing called for by dollar cost averaging may result in higher transaction costs compared to investing a lump sum of money once. Additionally, in a rising market, investors may miss out on potential gains by continuously purchasing at higher prices.

Even so, a huge advantage of this strategy is that it can reduce the overall impact of price volatility and lower the average cost per share. It’s definitely a low risk and long term approach, by having this in mind you can reduce anxiety and put a break on impulsive decision making against changing markets.

It’s also convenient in both bull market and bear market contexts. If there is a bull market, previously acquired stocks get revalorized, it’s still the same amount, but now they are worth more. And if there is a bear market, dollar cost averaging allows you to buy more quantity of the active at a lower price.

Lastly, a major advantage for the investor using DCA is not having to make a decision on a day to day basis about the best time to invest the funds. Its simplicity makes DCA a good choice for those beginners looking to develop habitual or automated regular investing.

Investing in the wrong moment has proven to be very expensive for the investor, if there is a crash in the market after the investing moment it could take several years to recover from it. The stock market crashed in 2000, 2008 and 2020, roughly once every seven years. So we certainly know that the market will crash from time to time but the specific moment or year is impossible to predict. This is the main reason why DCA it’s so important.

Peter Lynch once said “I know we´ve had 96 years of century and the market´s fallen 53 times, we have 53 declines of 10% or more, so 53 declines in 96 years, once every 2 years we have 10% decline. The 53 declines, 15 have been 25% or more, so 15 and 96 years about once every 6 years the market falls 25% or more. That’s what we call a bear market, you know that – and it’s going to happen. I don’t care when it’s going to happen. I would love to know, obviously it would be very useful to know when it’s going to happen. Doesn’t make any difference to me, corporate profits are going to be a lot higher 8 years from now, a lot higher 16 years from now, a lot higher 30 years from now. That’s what I deal with.”

This is what smart and good investors do, they don’t try to predict the unpredictable. Just avoid entering with the whole investment in the wrong moment by doing DCA and that’s it, you will avoid the pains caused by market volatility.

Conclusion

To conclude, we have made clear that the investment strategy of dollar cost averaging can be used by any investor who wants to take advantage of its benefits. You can mitigate the impact of market volatility, reduce the stress caused by trying to predict the unpredictable movements of the market and potentially benefit from lower average costs per share over time. Also, by spreading out investments over regular intervals, you can harness the power of compounding and smooth out the effects of market fluctuations.

While it may not guarantee substantial short term gains, its long term benefits are undeniable, making it a valuable tool for investors looking to build wealth steadily over time. Through consistent and disciplined investing, DCA has shown good long term results in a wide range of investments.

Dollar cost averaging turns out to be especially useful to beginning investors who don’t want to take the risky decision of picking the most opportune moments to buy (which by the way, we consider no one in the world, not even a sophisticated algorithm, can consistently and accurately predict the best moment to buy or sell).

It’s a reliable strategy for individuals seeking to navigate the complexities of investing while minimizing risk.