You’ve probably read or heard the terms “value investing” or “value stocks”. Even we, the Boring Investment team, tend to use these concepts to categorize the kind of investments that we consider suitable for anybody looking to become wealthy by putting their money to work for them.

But… What are value stocks? How do you recognize them? Can beginners invest in value stocks or are they reserved to experts? Today, we aim to answer these questions by showing you how to identify value stocks for beginners.

What Are Value Stocks?

Definition and key characteristics

Let’s start by defining the key term: value stocks are stocks that are trading for less than their true value according to the company’s fundamentals. The stock market sometimes undervalues good companies, often due to short-term factors like negative headlines or broader market trends.

So, value stocks are fundamentally sound companies whose share prices are low compared to what they are able to generate (in terms of profitability) due to market or sector-related events. Nevertheless, investors who analyze the companies anticipate that the share price will eventually increase due to the attractiveness of their underlying fundamentals.

Value vs. growth stocks

Value stocks tend to be more stable. Even when they might be undervalued, they are typically established companies with solid fundamentals, stable earnings, strong balance sheets, and a history of consistent performance – making them attractive for long-term investors looking for steady returns. This makes them less risky than growth stocks and a safer bet, especially during periods of market volatility or inflation.

On the other hand, growth stocks tend to have explosive growth potential. They belong to companies that are expanding rapidly, often reinvesting profits to fuel further growth (rather than paying dividends). While growth stocks can offer high returns, they are usually priced on speculation and rely on future earnings potential rather than current financial strength.

Why are growth stocks riskier than Value stocks?

From the previously said, it follows that growth stocks tend to be riskier because their valuations are often based on optimistic future projections rather than current earnings.

Growth stocks are more sensitive to market fluctuations and economic downturns, as investors may shift toward safer assets when uncertainty arises. In contrast, value stocks are generally less volatile because they are backed by tangible financial strength, making them a more stable investment option.

To understand this point, Benjamin Graham’s concept of margin of safety is very useful. It’s the difference between a stock’s price and its intrinsic value. The further a stock’s price is below its intrinsic value, the greater the margin of safety against future uncertainty and the greater the stock’s resiliency to market downturns.

Let’s examine, for example, the case of Tesla stocks, which plunged by over 50% from December 2024 to March 2025, a dramatic collapse that has stunned shareholders. In mid-December 2024, Tesla traded near an all-time high of around $480 per share; by early March 2025, it had sunk to roughly $220. This wipeout erased over $800 billion in market value.

This shows that volatility is the price of admission with growth stocks like Tesla. Investors who rely on these types of stocks -usually endorsed on the speculation and hype of the tech sector- have learned the bad way that when a stock’s price starts far outrunning its fundamentals, as Tesla’s did, it probably won’t be sustainable.

Key Metrics to Identify Value Stocks

We’ve talked about analyzing company’s fundamentals to recognize value stocks, at Boring Investment we use a reliable formula successfully tested to determine which stocks are worth investing in and when.

These are some elements you could have in consideration when looking for value stocks:

Price-to-Earnings (P/E) Ratio: The Price-to-Earnings (P/E) ratio is a key valuation metric used to assess how much investors are willing to pay for each dollar of a company’s earnings. It is calculated by dividing the stock price by the company’s earnings per share (EPS). A lower P/E ratio may indicate that a stock is undervalued compared to its earnings, making it a potential value investment. However, it is important to compare P/E ratios within the same industry, as different sectors tend to have varying average ratios.

Price-to-Book (P/B) Ratio: The Price-to-Book (P/B) ratio compares a company’s market price to its book value, which represents its net assets. This ratio is calculated by dividing the stock price per share by the book value per share. A P/B ratio below 1 suggests that a stock may be undervalued, meaning the company is trading for less than its actual net worth. Investors often use the P/B ratio to identify value stocks with strong assets relative to their market price.

Dividend Yield: Dividend yield measures the return investors receive in the form of dividends relative to a stock’s price. It is calculated by dividing the annual dividend per share by the stock price. A higher dividend yield can be attractive to value investors seeking steady income, especially in well-established companies with a history of consistent payouts. However, an extremely high yield may indicate financial distress, so it is crucial to analyze the company’s ability to sustain dividends over time.

Return on Invested Capital (ROIC): Return on Invested Capital (ROIC) measures how efficiently a company uses its capital to generate profits. It is calculated by dividing net operating profit after taxes (NOPAT) by total invested capital. A high ROIC indicates that a company is using its resources effectively to generate strong returns, which is a key characteristic of high-quality value stocks. Investors use ROIC to identify businesses with sustainable competitive advantages and efficient capital allocation.

Earnings Yield: Earnings yield is the inverse of the P/E ratio and is calculated by dividing a company’s earnings per share by its stock price. It represents the percentage return an investor would theoretically earn if the company’s profits were distributed as earnings. A high earnings yield suggests that a stock may be undervalued, making it an appealing option for value investors looking for stocks with strong income potential relative to their price.

Debt-to-Equity (D/E) Ratio: The Debt-to-Equity (D/E) ratio evaluates a company’s financial leverage by comparing its total debt to its shareholders’ equity. A lower ratio suggests a more financially stable company with less reliance on borrowing, which is often desirable for value investors looking for low-risk opportunities. Conversely, a high D/E ratio may indicate excessive debt, which can increase financial risk, especially during economic downturns.

Free Cash Flow (FCF): Free cash flow (FCF) represents the cash a company generates after covering its capital expenditures. It is a crucial measure of financial health, as it indicates a company’s ability to reinvest in growth, pay dividends, or reduce debt. Companies with strong free cash flow are often attractive value investments, as they have greater flexibility to weather economic downturns and return value to shareholders.

Stock Searcher

If you don’t know how or where to start with the fundamentals analysis, check our stock searcher where you can verify if your investment idea or stock in your portfolio is the best option compared to peers.

A value trap occurs when a stock appears to be undervalued based on traditional valuation metrics (such as the previously described) but is actually cheap for a reason – usually due to fundamental business weaknesses or declining future prospects. Investors who mistake these struggling companies for true value stocks may end up holding onto stocks that continue to lose value.

Even when ratios like price-to-earnings (P/E) or price-to-book (P/B) are promising, there may be long-term structural weaknesses. Therefore, before investing, it’s crucial to analyze financial health, industry trends, and management quality to distinguish between a genuine opportunity and a stock that will keep losing value.

How to avoid them with Boring Investing

To avoid these value traps, we recommend you to use our platform. Because it utilizes a proprietary financial scoring system that thoroughly analyzes companies to ensure they have sustainable competitive advantages. One key metric we emphasize, for example, is Return on Invested Capital (ROIC), which serves as an indicator of management quality and a company’s ability to generate returns above its cost of capital. By having in consideration our data-driven analysis, you can confidently identify real value stocks and steer clear of companies that may seem like bargains but lack the fundamentals for long-term success.

Conclusion

Patience and Discipline in Value Investing

In the past, we’ve made emphasis on the psychological aspect of value investing. Identifying value stocks requires more than just understanding financial metrics – It demands patience and discipline. Value investing is a long-term strategy that will reward you if you are willing to wait for the market to recognize a stock’s true worth.

Short-term price fluctuations and market sentiment can create buying opportunities, but only those with the discipline to hold their positions through volatility can fully benefit. Avoid emotional decision-making and stay committed to fundamental analysis to distinguish between genuine value opportunities and potential value traps.

Patience is essential because undervalued stocks don’t always rebound immediately. It may take months or even years for the market to correct mispricing, but history has shown that disciplined and patient investors who focus on strong financials and sustainable business models are often rewarded over time.

By applying key valuation metrics, avoiding speculative hype, and maintaining a long-term perspective, beginners can build a solid foundation in value investing and increase their chances of long-term success.

If you are a beginner getting started in this fascinating world of investments, don’t wait any longer and join us!

When people think about investing, the word “risk” usually dominates the conversation. You’ve probably asked yourself:

“What if I lose money? What if I invest at the wrong time?”

But here’s something most people overlook: Risk is not absolute — it’s a function of time.

At Boring Investment, we dove deep into the historical data of the S&P 500 and found that if you invest with a long-term mindset — and use the right strategy — risk virtually disappears.

We have used S&P 500 index instead of Boring Investment stocks because of historical information availability (for S&P 500 data starts in 1950). However, in the article linked we compare S&P 500 index returns with Boring Investment strategy to show how you can beat the market when you don’t invest in “sexy” companies.

At the end of this article you’ll understand why we conclude that, if a robust investment strategy is followed, financial risk is almost zero when you invest for a sufficient number of year and forget to try to time the market.

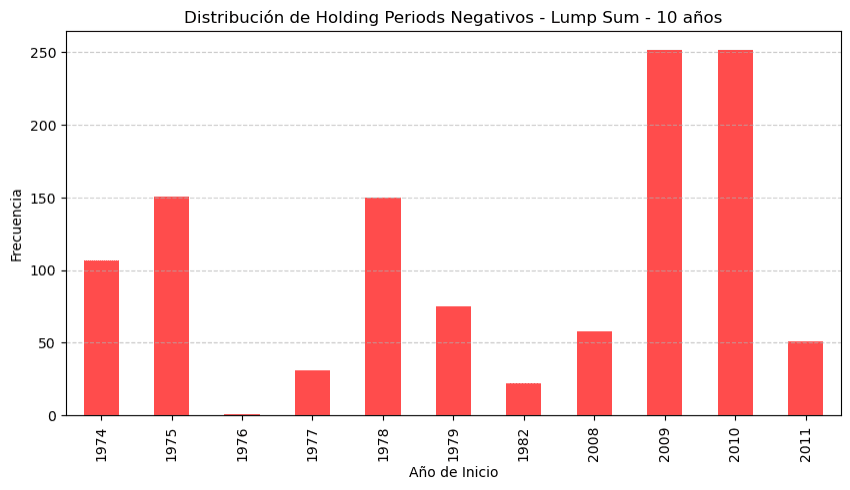

The Analysis: How Often Would You Have Lost Money in the S&P 500?

We analyzed data from 1950 to 2024 using two approaches:

Lump Sum: investing all at once at the beginning of the period.

Dollar Cost Averaging (DCA): investing gradually over time (daily, weekly, monthly, depending on the holding period).

We tested different investment horizons — from 1 day to 20 years — and calculated the percentage of time each strategy resulted in negative returns.

🔻 Percentage of Negative Periods – Lump Sum (investing all at once at the beginning of the period)

Holding Period

% of Losses

1 day

46.25%

5 days

43.09%

1 month

38.20%

1 year

25.59%

5 years

15.15%

10 years

6.09%

15 years

0.00%

20 years

0.00%

The longer your holding period, the lower the chance of losing money. After 15 years, there’s no historical precedent for a loss.

What Happens When You Use Dollar Cost Averaging (DCA)?

Here’s where it gets even better.

With DCA, where you invest periodically (investing same amount across time, e.g. monthly), the probability of loss drops significantly across all timeframes.

Holding Period

Lump Sum (%)

DCA (%)

1 day

46.25%

46.25%

5 days (DCA is applied daily)

43.09%

41.90%

10 days (DCA is applied daily)

40.82%

39.44%

1 month (DCA is applied weekly)

38.20%

37.02%

3 months (DCA is applied weekly)

33.28%

31.18%

6 months (DCA is applied weekly)

29.33%

27.24%

1 year (DCA is applied monthly)

25.59%

21.65%

3 years (DCA is applied monthly)

14.12%

11.26%

5 years (DCA is applied monthly)

15.15%

6.65%

7 years (DCA is applied monthly)

7.24%

0.48%

10 years (DCA is applied monthly)

6.09%

0.00%

15 years (DCA is applied monthly)

0.00%

0.00%

20 years (DCA is applied monthly)

0.00%

0.00%

🔵 Bottom Line: DCA Reduces Risk — Almost to Zero at 7 Years, and Literally to Zero After That

Dollar Cost Averaging doesn’t just reduce risk — it crushes it.

By 5 years, DCA already cuts your chance of loss in half compared to Lump Sum. By 7 years, the percentage of negative periods drops to just 0.48%.

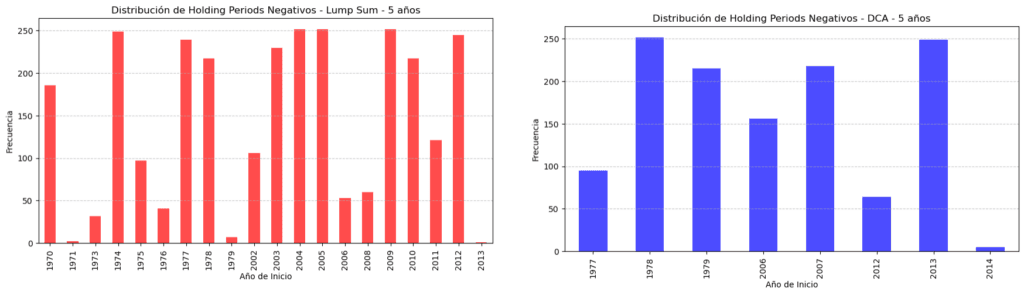

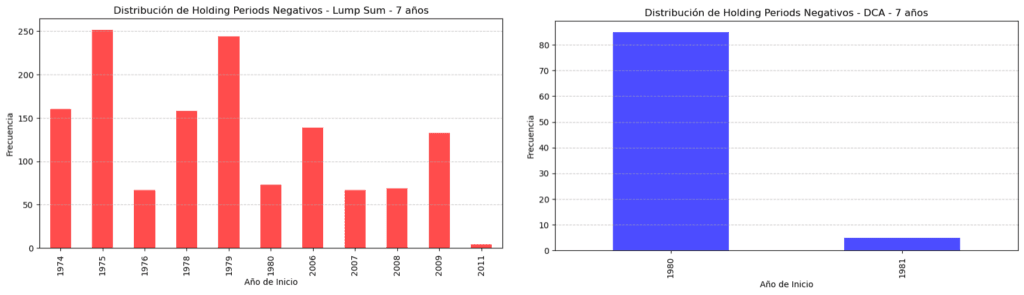

Why isn’t 7 years holding period zero? Two years explain it all: 1980 and 1981.

Out of all the data from 1950 to 2024, only two years — 1980 and 1981 — led to negative 7-year DCA returns.

Here’s what happened:

Inflation was out of control in the late 1970s, reaching over 14%.

The U.S. Federal Reserve, under Paul Volcker, raised interest rates above 20% to fight inflation.

This triggered two consecutive recessions in 1980 and 1981-82.

Markets struggled for years under tight monetary policy and slow economic recovery.

As a result, investors who started DCA in 1980 or 1981 experienced subdued returns over the following 7 years — just enough to end slightly negative.

But think about it — that’s 2 years out of 75.

In other words: 97.3% of the time, 7-year DCA investments were positive, and 100% of the time at 10 years or more.

How Many Years Actually Had Negative Periods?

Holding Period

Years Analyzed

Negative Years / Frequency – Lump Sum

Negative Years / Frequency – DCA

1 year

75

48 (64%)

35 (47%)

3 years

75

21 (28%)

13 (17%)

5 years

75

20 (27%)

8 (11%)

7 years

75

11 (15%)

2 (3%)

10 years

75

11 (15%)

0 (0%)

15 years

75

0 (0%)

0 (0%)

20 years

75

0 (0%)

0 (0%)

DCA slashes the number of years with negative outcomes — and makes long-term investing incredibly safe.

📊 Visualizing the Risk

Most losses happen during specific crises:

The stagflation of the 1970s

The Dot-com bubble (2000)

The 2008 financial crisis

The 2020 COVID crash

But if you stayed invested long enough, the market always recovered — and rewarded your patience.

Now, let’s add an important layer to our analysis, how about returns?

Full Results: Negative Returns & Annualized Performance

Holding Period

DCA % Negative

DCA Mean

DCA P25

DCA P50

DCA P75

1 day

46.26%

7.8%

-102.7%

12.4%

127.6%

5 days

41.91%

7.8%

-40.1%

15.5%

61.1%

10 days

39.49%

7.9%

-24.1%

14.2%

45.4%

1 month

37.06%

7.9%

-13.0%

12.7%

33.4%

3 months

31.28%

7.8%

-4.5%

10.1%

23.5%

6 months

27.43%

7.7%

-1.8%

9.9%

18.9%

1 year

21.95%

7.7%

1.3%

8.8%

16.7%

3 years

11.73%

7.5%

3.6%

8.6%

11.4%

5 years

7.12%

7.5%

2.5%

8.2%

11.2%

7 years

0.53%

7.3%

3.2%

8.3%

10.7%

10 years

0%

7.1%

3.7%

7.5%

10.4%

15 years

0%

7.0%

5.2%

6.7%

9.4%

20 years

0%

6.8%

5.1%

6.8%

8.3%

🏦 How Does This Compare to “Risk-Free” Treasury Bonds?

Let’s say the average 10-year Treasury Bond yields ~4% annually. It’s considered “risk-free” because of government backing.

But here’s the thing:

At 10 years, the S&P 500 with DCA never lost money historically.

And not only that — the median annual return was 7.5% (DCA), almost double the bond yield.

Even at P25 (worst quartile), returns were around 3.7%, almost matching bonds with equity upside.

Conclusion? Over long horizons, the stock market becomes practically “risk-free” in outcome, but with far better returns.

The real “risk” is not time — it’s short-term thinking.

Investing Risk = Time. Period.

This leads to a crucial insight:

Investment risk isn’t about volatility. It’s about time.

If there are zero 10-year periods with negative DCA returns, how risky is investing, really? Almost inexistent I would say.

The Real Question Isn’t “What’s Your Risk Tolerance?”

It’s this:

What’s your investment time horizon?

If you can ride out short-term noise, you don’t need to fear risk. Time is your best hedge.

Investing Isn’t About Timing. It’s About Enduring.

You won’t predict the market. But you don’t have to. All you need is a plan, consistency, and the discipline to hold through downturns.

At Boring Investment, we help you:

Invest safely and consistently, with minimal effort.

Use data, not emotions.

Let compound interest and time do the heavy lifting.

Ready to invest the boring (but effective) way?

👉 Try our Investment Platform to invest wisely theboringinvest.com 👉 Subscribe for more no-fluff, data-backed insights in the form below

In a previous article we taught you how to open an account in Interactive Brokers. The process of opening an account, although it may seem long or complicated, is actually very simple. That’s why today, we’ll show you some common questions related to frequent issues when opening an IBKR account that we aim to answer.

How long does it take to open an IKBR account?

On the one hand, it should take around 20 minutes of your time to fulfill the application with all your personal information required and account setup.

On the other hand, it usually takes 3 business days for the Interactive Brokers team to approve your application – if not, they will contact you to share what went wrong and why they are rejecting it.

It may take longer than expected if you submit blurry or incomplete documents, provide an address that doesn’t match your ID or miss required tax information (such as a TIN for U.S. taxpayers). So make sure you are accurate with the information you upload.

Note that you can always fund your application to prioritize its review. And if for any reason your application is not approved, the funds will be returned.

Why is it important to fund your account?

By funding your account, you are putting money in the broker. It enables access to trading and gets you ready to invest and generate profits. The initial deposit acts as the foundation of your trading activities and is necessary to begin using the platform.

Without funding, your IBKR account remains inactive, and you won’t be able to execute trades or invest in the various financial instruments. You may also find limited features or no trading data.

How do you know the funds are credited to your account?

The date funds will be credited to your account depending on the method of funds transfer you use. To check the latest status of your deposit you may choose any of the following.

View a recent Activity Statement for details on when your deposit will be available for trading.

Why can your application get rejected?

Interactive Brokers (IBKR) can reject account applications for several reasons, often tied to the applicant’s failure to meet certain eligibility criteria or incomplete application processes. Here are some common issues:

Incomplete or Incorrect Information: Applications with missing or incorrect details -such as errors in personal identification or address documentation- may be delayed or rejected. It’s crucial to ensure all required fields are filled out accurately and supported by valid documentation.

Failure to Meet Eligibility Requirements: Interactive Brokers has specific eligibility criteria depending on the account type and applicant’s country of residence. These may include minimum net worth, income requirements, or trading experience. Applicants who don’t meet these thresholds, particularly for professional or margin accounts, are likely to face rejection.

Issues with Documentation: If the applicant fails to provide acceptable proof of identity, address, or bank account information, the application can be delayed or denied. Similarly, discrepancies between submitted documents and the application details can lead to rejection.

Regulatory Restrictions: Some countries impose restrictions on accessing international brokerage services like IBKR. If regulatory compliance requirements aren’t met, the account may not be approved.

To avoid these issues, applicants should carefully review IBKR’s requirements, double-check the accuracy of their application, and promptly respond to any follow-up requests for additional information or clarification.

Are there residency restrictions?

Yes. While IBKR operates globally, certain countries may impose restrictions or additional requirements based on local regulations. Applicants from countries with strict financial compliance laws might face delays or additional documentation requests.

If Interactive Brokers doesn’t work in your country, don’t worry, you still can invest in reliable brokers: check our previous article about the Top Biggest Brokers for each Country.

Problems with the fiscal number or TIN

TIN means tax identification number, and it is a unique identifier assigned to individuals and entities for tax purposes.

You may find some issues related to the following aspects:

Invalid TIN Information: typographical errors, invalid TIN formats or mismatch with official records (remember that The TIN provided must match the records held by the relevant tax authority).

Missing TIN: Applicants that are minors or non-taxpayers in their home country might not have a TIN, also, certain jurisdictions issue temporary TINs, which might not be accepted by IBKR as valid identification.

International Tax Residency: Applicants with tax residency in multiple countries might be required to provide all relevant TINs. If a user is residing outside their home country, providing a TIN from a different jurisdiction might not align with their stated residency.

FATCA/CRS Compliance Issues: On the one hand, FATCA (Foreign Account Tax Compliance Act) is a U.S. regulation aimed at preventing tax evasion by U.S. taxpayers holding financial assets outside the country, so for U.S. citizens or residents, failure to provide a valid Social Security Number (SSN) instead of a TIN may lead to compliance issues. On the other hand, CRS (Common Reporting Standard) is an international framework for the automatic exchange of tax information between countries, so non-U.S. residents need to provide accurate TINs to comply with international tax reporting regulations.

Tax forms

During the account-opening process, IBKR will ask for your tax status. Based on your residency and citizenship, you will be prompted to complete the W-8BEN or W-9 form electronically.

The W-8BEN form certifies that you are not a U.S. citizen or resident for tax purposes, and it prevents unnecessary withholding tax on income that might apply to U.S. based investments. If incomplete or not submitted, IBKR may apply the default withholding tax rate of 30% to applicable U.S.-source income, even if you’re eligible for a reduced rate.

The W-9 form is required for U.S. residents or citizens, and it provides IBKR with your Taxpayer Identification Number (TIN), such as your Social Security Number (SSN) or Employer Identification Number (EIN). Failing to submit this form may result in the account being flagged, and the IRS may impose backup withholding on income (currently at 24%).

How to make a transfer within the USA to Interactive Brokers?

From the Client Portal go to the Transfer & Funds section and select Transfer Funds

Choose the deposit type and the option Bank Wire (US) for transfers within the United States

IBKR will provide the necessary banking details: name of the receiving bank, routing number (might be ACH or ABA indifferently), IBKR’s account number and your unique reference code (essential to identify your transfer)

Make the transfer from your bank account with the provided details – make sure you include the unique reference code in the notes or description field

Check the transfer status from the IKBR Transaction History section. Note that domestic transfers within the USA usually process within 1-2 business days.

How to deposit EUR to Interactive Brokers?

IBKR`s bank account for EUR is eligible to receive EUR transfers either via SEPA or International Bank Transfer (SWIFT).

They will provide you with our IBAN (International Bank Account Number) and the SWIFT code of their bank account upon completing the deposit notification in Client Portal.

If your bank is located within the EU (and certain other countries) you will likely use the SEPA transfer method. Otherwise, you will need to use International Bank Transfer (SWIFT) method instead.

How to transfer funds out of IBKR?

Log into Client Portal

Select Transfer & Pay followed by Transfer Funds

Click Make a Withdrawal

Select an instruction from the Saved Withdrawal Information section, or select the Currency from the currency list to see eligible methods

Click Use this Method next to your desired method and complete the subsequent screens to complete your request.

Are there requirements in order to qualify for trading permissions?

Yes. The trading permissions request can take 24 to 48 hours for approval. However, in order to be approved, your financial profile (e.g. age, liquid net worth, investment objectives, product knowledge and prior trading experience) must meet IKBR qualifications.

How to update your financial profile?

Log into Client Portal

Click on the User menu (head and shoulders icon in the top right corner) followed by Settings

Under Account Settings find the Account Profile section

Click on Financial Information, rectify your information and confirm.

Where to get help?

If you are having troubles with the process, you can always ask for guidance from the IKBR team or from us, Boring Investment team.

In this article, we will explore the largest brokers across major economies worldwide, so you can know where to invest by having in consideration the top biggest brokers for each country.

The global landscape of brokers is highly diverse, with each country presenting its own set of dominant players shaped by local regulations, market dynamics, and investor preferences.

Understanding the biggest brokers in different regions helps investors make informed decisions about where to invest. It’s useful for finding a reputable broker within your own country that provides security and confidence. It’s often beneficial to invest through brokers based in your own country, as not all brokers have a presence in every nation, and each country typically has a unique regulatory and tax framework.

If you are just getting started in this passionate world of investments and don’t know how to select your broker or open a broker account, check our first steps section – where we show you how to start investing in a simple way, accessible to everyone.

Of course, we couldn’t consider every country in the world, so we have made a thoughtful selection by including 14 countries in our analysis as paradigms of the diversity of brokerage offer. These are the top biggest brokers for each country.

USA

JAPAN

UK

GERMANY

INDIA

CHINA

BRAZIL

Vanguard Group

Nomura Securities

Interactive Brokers

Deutsche Bank

Zerodha

Futu Holdings

XP Investi-mentos

Charles Schwab

SBI Securities

Saxo

Flatex DEGIRO

ICICI Direct

Tiger Brokers

BTG Pactual

Fidelity Investments

Rakuten Securities

eToro

OnVista Bank

HDFC Securities

CICC

ModalMais

J.P. Morgan

Monex Group

XTB

DKB

Kotak Securities

GF Securities

Rico Investi-mentos

Merrill Wealth Managmnt.

Mizuho Securities

Plus500

Comdirect

Upstox

Haitong Securities

Clear Corretora

AUSTRALIA

CANADA

MEXICO

SOUTH AFRICA

TURKEY

SPAIN

FRANCE

CommSec

Questrade

GBM

Standard Bank Online Share Trading

Garanti BBVA Yatırım

Renta 4 Banco

Boursorama

IG Group

RBC Direct Investing

Actinver

EasyEquities

İş Yatırım

Bankinter Broker

BNP Paribas Personal Investors

CMC Markets

TD Direct Investing

Monex

PSG Wealth

Ziraat Yatırım

Self Bank by Singular Bank

Crédit Agricole Titres

SelfWealth

Scotia iTRADE

Citibanamex

Nedbank Private Wealth

Halk Yatırım

BBVA Trader

SG Markets

NabTrade

BMO InvestorLine

Banorte

EasyEquities

Yapı Kredi Yatırım

Santander

Fortuneo

As you can see, there is a high-variety of brokers around the five continents. Each with its own particularities in trading preferences, regulatory requirements, and investors behavior.

Each country’s legal and tax frameworks may require specific conditions, so in general, it’s preferable to select a broker with local presence in your country of fiscal residence.

But now, how do we determine the biggest brokers? By having in consideration the following aspects:

Parameters to measure the size of brokers

Assets Under Management (AUM): The total value of assets that the broker manages for its clients. A larger AUM typically indicates more trust from clients and a strong reputation in the market.

Number of Clients/Accounts: The total number of active clients or brokerage accounts provides insight into the firm’s client base size. Larger brokers generally have more accounts, indicating widespread use by investors.

Revenue and Profitability: A broker’s financial performance, including total revenue and profit margins, reflects its operational strength. Revenue comes from various sources such as trading commissions, advisory fees, and interest on margin accounts.

Market Share: The broker’s share of the trading market, both in terms of retail and institutional clients, is another indicator of its dominance. High market share often corresponds with a firm’s size and influence.

Trading Volume: The volume of trades executed by the broker indicates its activity level. Higher trading volume, especially across different asset classes (stocks, bonds, etc.), highlights the broker’s ability to handle a large number of transactions efficiently.

Geographic Reach: A broker’s global footprint, including the number of countries it operates in, also affects its size. Brokers with a presence in multiple regions often have broader access to capital markets and a more diverse client base.

Technology and Platform Infrastructure: In today’s digital world, the technology stack and quality of trading platforms (user experience, speed, accessibility) are increasingly important. Brokers that invest heavily in cutting-edge technology and user-friendly platforms tend to grow faster.

If you are finding this information valuable, check some of our previous articles!

Why is this useful?

You may be wondering how this information can help you make informed investment decisions in a global context.

When considering global investment strategies, understanding the size and impact of brokerage firms in different countries is a key advantage. Knowing the largest brokers by the previously mentioned parameters, can help investors assess credibility, stability, pricing and potential opportunities, not only for portfolio expansion across borders, but also for investing in your own country.

Size matters because larger brokers often offer more resources, tools, and international access to investment markets, providing more diverse and stable platforms for trading.

Evaluating broker size helps in assessing stability, as larger firms generally have more capital reserves and can endure market fluctuations more effectively. In times of financial instability, larger brokers can provide an extra layer of security by being less vulnerable to liquidity risks compared to smaller firms. For global investors, this can be particularly relevant when considering economic downturns or inflation spikes in particular regions. Learn how to beat inflation.

Aside from stability, broker size also influences pricing. Larger brokers often offer more competitive fees and spreads, thanks to their ability to leverage scale and negotiate better prices.

Understanding the biggest brokers in a given market can also be key to accessing new investment opportunities. Large brokers are typically at the forefront of innovation. By identifying the top players in your country, you can align yourself with firms that are leading in terms of technology and product development.

CONCLUSION

In the global context, understanding the top biggest brokers for each country, offers invaluable insight for investors seeking reliable and comprehensive financial services. We hope that knowing the top brokers for each country from the table can help you find a big and reliable broker in your country to invest in a safe and simple manner.

As discussed under the “Parameters to measure the size of brokers,” factors such as assets under management, number of clients, revenue and profitability, market share, trading volume, global reach, and technological capabilities are critical benchmarks to determine the size and reliability of a brokerage firm.

Additionally, this information is highly useful for investors looking to invest in local brokers, or even enter foreign markets and diversify their portfolios. As explored in the section “Why is this useful?” knowing the largest brokers enables investors to identify firms with robust financial stability, a solid reputation, and a wide range of investment products and services.

Ultimately, knowing and having access to these brokers provides investors with greater security, more diversified opportunities, and a pathway to navigate international and national markets with confidence.

We can help you in the process of becoming wealthy. Join us! To learn how and where to invest your money: https://theboringinvest.com/

To invest, it’s necessary to open a broker account where you can make transactions safely and dynamicallyfacilitated by a unified platform. The offer of brokers is increasing with the passing of time and the popularization of investments as a way to become wealthy. Today, we will focus on how to open an account in Interactive Brokers with 6 easy-to-follow steps.

Why Interactive Brokers? We believe it’s a reliable broker where your information and activity will be protected. It’s very intuitive to use and since the beginning of your experience, you’ll realize they take care of their users with the responsibility and seriousness it requires.

If you are just getting started in this passionate world of investments and don’t know how to select your broker or open a broker account, check our first steps section – where we show you how to start to invest in a simple way, accessible to everyone.

STEP 1: Create an account

Here, you just have to create a username and password, and confirm your email address from your email account. After that, you can start completing the application.

APPLICATION

STEP 2: Select an Account Type

In the first section of the application, you have to select the account type that’s more convenient for your needs and goals. The decision will depend on whether you’re applying as an individual making an occasional investment, a professional and frequent trader, or an institutional investor. Let’s suppose you choose the most common individual account, it’s the best suited account for those unexperienced who want to start investing from savings.

Once you’ve selected the account type best suited for you, it’s time to provide your personal information.

STEP 3: About you

In this instance, you have to complete a few steps that contemplate the following information: contact and personal data; identification (ID); employment status and source of wealth; base currency; and three security questions to make your account safer.

By completing your employment status, you’re sharing your occupational situation, it can be employed, self employed, retired, unemployed, etc. Your response might determine your source of wealth selection; if you are employed, the salary option (“income from employment”) will be pre-selected, but you can choose as many as you please as long as they are verifiable sources of wealth for you.

STEP 4: Regulatory

Next, you’ll go through the regulatory section, where you will be required to answer questions related to your investment goals, risk tolerance, and trading experience.

In this step, you configure your trading account by selecting an account type between cash, margin or portfolio margin. If you select margin and portfolio margin there are more requirements that are related to your financial information. So the most simple option is cash – unless you are planning to invest with leverage or other advanced investment strategies.

By providing your income and net worth as well as your investment objectives and intended purpose of trading, Interactive Brokers (IB) make sure you are legally capable to trade the assets of your choice.

You’ll be asked to set your account preferences, indicating your trading experience and permissions (such as access to global markets), so IB can assess your eligibility and tailor the platform to suit your needs, ensuring compliance with regulatory standards.

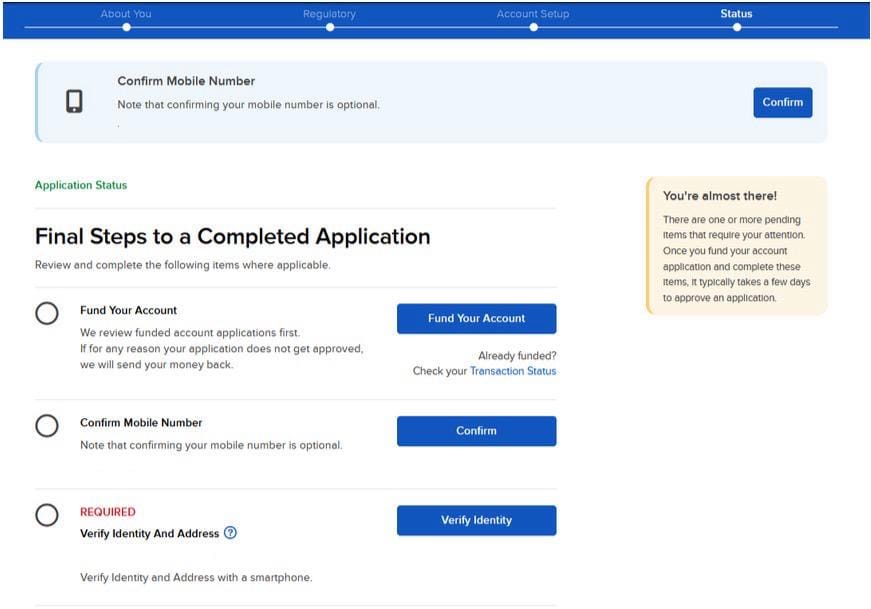

STEP 5: Account Setup

You’re almost done! The legal aspect is taken care of here: You accept the terms and conditions by reviewing and agreeing to the necessary legal disclosures and documents.

Once you verify your identity and address with a selfie or photo of your id and with your GPS location or another document of your choice, your application will be submitted and approved in a few days.

Finally, when all the steps are completed, IB will review your application. You can monitor your account status directly from your dashboard, where you’ll receive updates on the approval process. And you’ll receive an email notification to confirm that your account is active and ready for use.

Once you have your account approved you’ll be ready to start investing. If you are not sure about how to do it, check our previous article on how to invest in stocks for beginners.

CONCLUSION

In conclusion, opening an Interactive Brokers account is a straightforward process that can be completed in a few steps, from creating an account to receiving the final approval. By carefully selecting your account type, providing accurate personal and financial information, and setting up your preferences, you can tailor the platform to suit your investment needs. Once your account is approved, you gain access to a wide range of global markets and trading tools, making IB a powerful platform for both new and experienced investors.

If you have any doubt about the beginning or the investment process itself, don’t wait any longer and Schedule time with an expert.